How Is Your LGM Indemnity Calculated?

Today’s market constantly changes, making it difficult for farmers to lock down the profits needed to keep their operations running. Feed and livestock prices are volatile, and unexpected market price drops can leave you feeling like the rug has been pulled out from under you.

But you aren’t alone. Risk management solutions can provide peace of mind by creating a safety net for your revenue. By offering a gross margin guarantee, Livestock Gross Margin (LGM) secures your bottom line, protecting your operation against sudden changes to feed and cattle prices.

What does the settlement process look like, and what happens if market prices are down when you’re ready to sell your livestock? Let’s briefly recap LGM and look deeper into the LGM settlement process.

What is LGM?

LGM is a Federal Crop Insurance Corporation-based insurance program designed to help producers protect their operations against today’s volatile market. It’s impossible to predict what tomorrow’s market will look like, but LGM offers a gross margin guarantee, which protects producers against a rise in the cost of feed, a rise in feeder cattle costs, and a decline in live cattle prices.

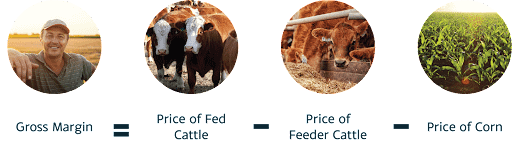

LGM secures your operation’s profit by accounting for the expected price margin between your cattle’s market value and the feed cost. You can calculate your gross margin by subtracting the cost of feeder cattle and feed from the market value of your herd.

When you purchase an LGM policy, your coverage is based on the expected profit margin of your cattle when you purchase your plan. If prices change and shrink your actual gross margin when you take your herd to market, LGM will cover the difference so you won’t lose out on key profit.

How Are Indemnities Calculated?

Once your endorsement period ends and you’ve sold your cattle, the settlement process begins. You may be entitled to an indemnity depending on the gross margin you receive from selling your livestock.

An indemnity is the payment you receive that covers the difference between your actual gross margin and your policy’s expected gross margin. Simply put, if the actual gross margin you receive at the market is less than your expected gross margin, you will receive an indemnity that bridges the gap. You will not receive an indemnity if your actual gross margin is higher than your coverage price.

Let’s take a look at a brief example:

- A cattle producer purchases an LGM policy with an expected gross margin of $600 per head; his deductible is $10 per head. When he goes to market, the cost of corn is up, and the price of live cattle is down. In this instance, he receives only $400 per head. Since his actual gross margin is less than his expected gross margin, he’s entitled to an indemnity, which accounts for the difference between his actual and expected gross margins, minus his deductible. He’ll receive a net indemnity of $190 per head.

- In another case, the same producer goes to market when the cost of corn is down, and live cattle prices are up. This time, he receives an actual gross margin of $700 per head when he goes to market. He will not receive an indemnity because his actual gross margin was higher than his covered price.

When market prices make unexpected changes, preparing for the worst is essential. LGM helps secure your bottom line, but the ceiling remains wide open. When the market is up, you’ll benefit from high prices, and LGM creates a safety net to ensure that your investment is secured against potential downturns.

In our example, the cattle producer retained revenue by receiving his indemnity when the market was down.

Getting Started With LGM

Market volatility can often feel overwhelming, but there are simple solutions designed to help you secure your investments. You work hard to raise your livestock, so you shouldn’t have to settle for less.

LGM provides security for producers at all stages of the production cycle, with flexible coverage options so you can tailor a plan that meets your operation’s unique needs.

Learn what sets LGM apart from other risk management solutions:

- Premium rates are subsidized by the government, making it a more affordable option.

- LGM can be used as a standalone policy or with other tools.

- Flexible coverage periods allow you to select a timeframe that aligns with your production cycle.

- LGM is backed by the Federal Crop Insurance Corporation, providing security and reliability to producers like you.