What is

Livestock Gross Margin?

Managing risk can be confusing, complicated, and unpredictable. Where do you start? What are your options?

What is Livestock Gross Margin?

Livestock Gross Margin (LGM) is a Federal Crop Insurance Corporation-based insurance program which guarantees that you’ll receive a certain gross margin for your herd at the end of an 11-month insurance period. It factors the market value of your herd minus the costs of feeder cattle and feed.

How Can LGM Protect Your Operation?

Why Should you Choose LGM?

- Protection > LGM insurance provides protection to cattle producers against declines in cattle prices and increases in feed costs.

- Expected Profit Margin > The insurance is based on the expected profit margin of the cattle, rather than the actual price of the cattle, making it a risk management tool for the profitability of the operation.

- Margin > It covers the margin between the market value of the cattle & the cost of feed, which is a significant expense in cattle production.

- Flexible Coverage Period > Coverage periods are flexible, allowing producers to select a time frame that aligns with their production cycle.

- Lock in Profits > LGM allows producers to lock in a minimum acceptable profit margin, reducing uncertainty and providing peace of mind.

- Uses > It can be used as a stand-alone policy or in conjunction with other risk management tools.

- Premium Rates > Premium rates are subsidized by the government, making it a more affordable option for producers.

- Tailor to your Needs > LGM insurance is designed to be flexible and can be tailored to the unique needs of individual cattle producers.

- Coverage > It can provide coverage for both fed cattle and feeder cattle, providing protection at different stages of the production cycle.

- Secure and Reliable > LGM insurance is backed by the Federal Crop Insurance Corporation (FCIC), which provides a level of security and reliability for producers.

Top Benefits of LGM Coverage

Protect Your Margin from Above

And Below

Get Flexibility in Your Coverage

LGM’s options include:

- Customizable timeframes

- Flexible coverage levels

- Standalone policies, or policies that work alongside other risk management tools such a futures contracts and LRP

Each producer has different risk management needs. When you choose Stockguard for LGM, we’ll work together to tailor your coverage to match your risk tolerance, budget, and needs.

What is the difference between LGM and LRP?

Whereas LGM covers the price of the gross margin per head, LRP uses the Chicago Mercantile Exchange’s contract prices to insure the price of sold livestock. While LRP is typically a better fit for cow-calf operations, LGM is the preferred option for most feedlot operations.

LGM VS CME Contracts

Livestock Gross Margin (LGM) insurance and CME contracts are two different tools that are used by cattle producers to manage risk in the cattle market. Here are some differences between the two:

LGM:

- Covers the expected profit margin

- Insures against the risk of declining cattle prices or increased feed costs

- Requires a premium payment

- Premiums are subsidized by the government

- Flexible coverage periods

- Customizable coverage plans based on your needs

- Pays out based on the difference between the expected profit margin and the actual profit margin

CME:

- Covers the actual price

- Only covers the risk of declining cattle prices

- Requires upfront payment of the full contract value

- No subsidies

- Fixed expiration dates

- Standardized contracts with limited options

- Pays out based on the difference between the contract price and the current market price

Overall, LGM insurance and CME contracts are two different tools that cattle producers can use to manage risk in the cattle market. LGM insurance provides protection against declines in cattle prices and increases in feed costs, while CME contracts provide protection only against declines in cattle prices.

Getting Started with LGM

We know things can get complicated so let's break it down!

Select Options

Place Order

Guard your investment

Example

In September 2015, an Oklohoma producer buys LGM – Yearling Finishing insurance coverage to market 100 head in March 2016

- Insurance period is October 2015 through August 2016

- Deductible selected is $10/head

- Producer pays a premium of $85/head

- Expected Gross Margin for March is $130.80/head

Example from “Livestock Gross Margin & Livestock Risk Protection.” Oklahoma State University

You can find the needed information in regard to the coverage listed on the RMA website or through our portal at portal.stockguard.io

Remember – finishing yearlings is designed for 750-pound feeder cattle to be finished to 1,250 pounds, and uses a fixed corn amount of 50 bushels.

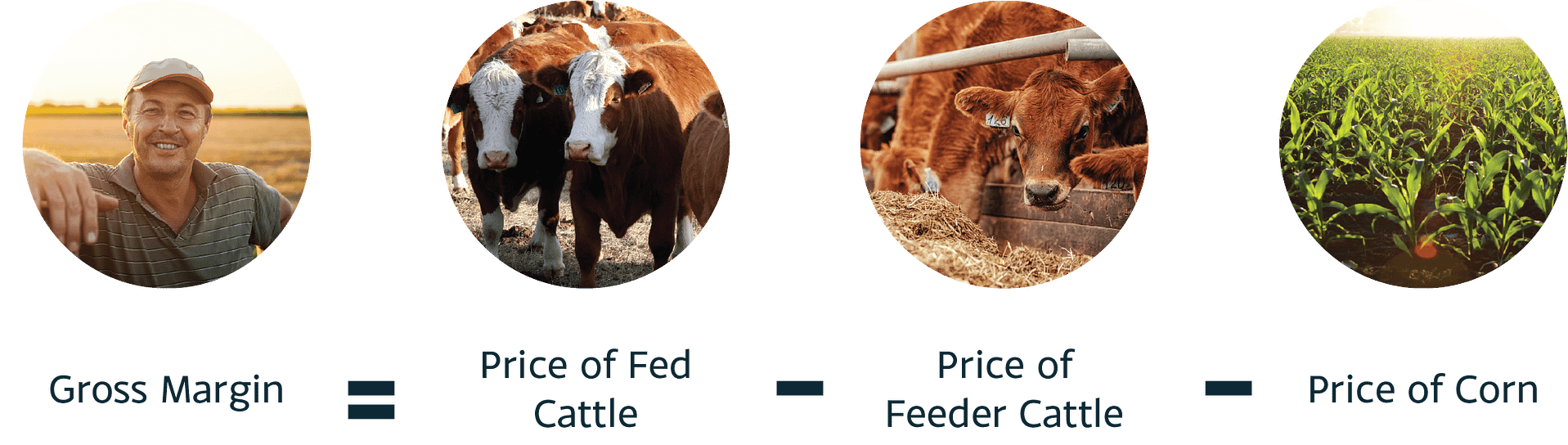

How to Calculate Expected Gross Margin

Expected Gross Margin = (12.5 x FedCattle$) – (7.5 x FeederCattle$) – (50bu x Corn$)

Expected Gross Margin equals 12.5 (with the 12.5 representing the finished weight of 1250 pounds) times the futures price of Fed Cattle minus 7.5 (with 7.5 representing 750 pound beginning weight) times the futures price of feeder cattle minus 50 bushel corn times the futures corn price.

Gross Margin and Indemnities

RMA calculates Actual Gross Margin of $7.43/head

Indemnity (per head) = ((Expected Gross Margin – Deductible) – Actual Gross Margin)

= (($130.80 – $10 ) – $7.43) = $113.37

Total Indemnity = $113 x 100 head = $11,300

Total Premium = $85 x 20 head = $85,00

Total net gain = $11,300 – $8,500 = $2,800

In March the producer markets 100 head. In this situation the actual gross margin is calculated at $7.43/head and the producer will be entitled to an indemnity calculated as shown below: